1. Single Option Strategies

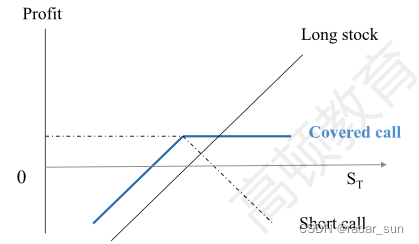

Covered Call(Long Stock + Short Call)

-

S

T

<

X

S_T<X

ST?<X

- Short call: c c c

- Long stock: S T ? S 0 S_T-S_0 ST??S0?

- 合计 c + S T ? S 0 c+S_T-S_0 c+ST??S0?

-

S

T

≥

X

S_T \geq X

ST?≥X

- Short call: c ? ( S T ? X ) c-(S_T-X) c?(ST??X)

- Long stock: S T ? S 0 S_T-S_0 ST??S0?

- 合计 c + X ? S 0 c +X-S_0 c+X?S0?

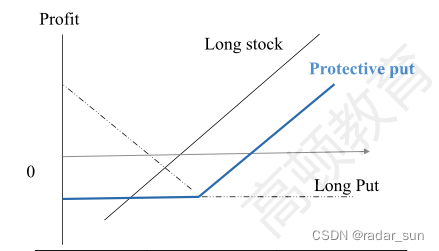

Protective Put(Long Stock + Long Put)

-

S

T

≥

X

S_T \geq X

ST?≥X

- Long call: ? p -p ?p

- Long stock: S T ? S 0 S_T-S_0 ST??S0?

- 合计 S T ? S 0 ? p S_T-S_0-p ST??S0??p

-

S

T

<

X

S_T < X

ST?<X

- Short call: ( X ? S T ) ? p (X-S_T)-p (X?ST?)?p

- Long stock: S T ? S 0 S_T-S_0 ST??S0?

- 合计 X ? S 0 ? p X-S_0-p X?S0??p

Principal Protected Notes(PPNs)

Principal protected note: a security created from a single option such that the investor benefits from any gain of a specified portfolio without the risk of losses.

- Long a three-year zero-coupon bond that will pay USD 10,000 in three years.

- Long a three-year call option on a portfolio, which is currently worth USD 10,000 with a strike price of USD 10,000.

2. Spread Trading Strategies

画图的时候记得strike price与option price的关系

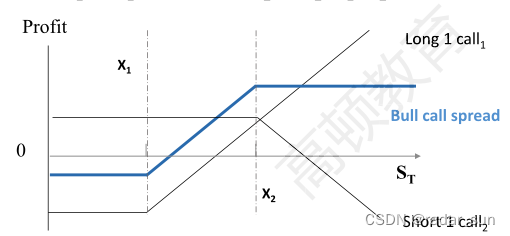

Bull Call Spread

- Long 1 C a l l 1 Call_1 Call1? at X 1 X_1 X1? + Short 1 C a l l 2 Call_2 Call2? at X 2 X_2 X2?

-

X

1

<

X

2

X_1<X_2

X1?<X2?

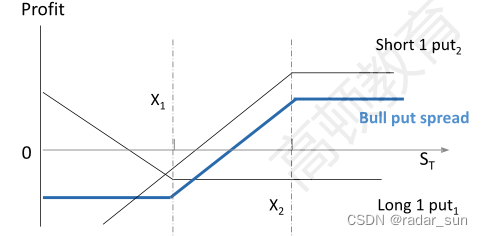

Bull Put Spread

- Long 1 p u t 1 put_1 put1? at X 1 X_1 X1? + Short 1 p u t 2 put_2 put2? at X 2 X_2 X2?,

-

X

1

<

X

2

X_1<X_2

X1?<X2?

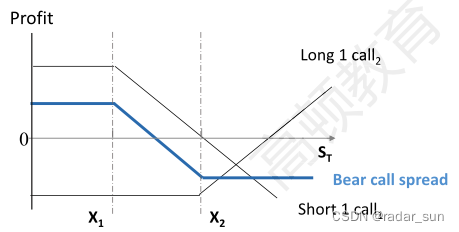

Bear Call Spread

- Short 1 C a l l 1 Call_1 Call1? at X 1 X_1 X1? + Long 1 C a l l 2 Call_2 Call2? at X 2 X_2 X2?

-

X

1

<

X

2

X_1<X_2

X1?<X2?

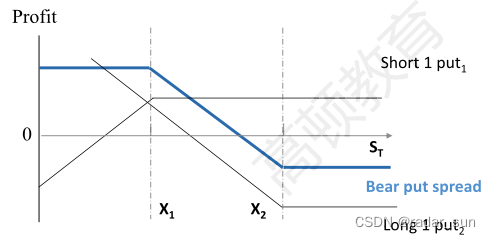

Bear Put Spread

- Short 1 p u t 1 put_1 put1? at X 1 X_1 X1? + Long 1 p u t 2 put_2 put2? at X 2 X_2 X2?

-

X

1

<

X

2

X_1<X_2

X1?<X2?

Box Spread - Bull call spread + Bear put spread

- Strike prices and Times to maturity used for the bull spread are the same as those used for the bear spread.

- Under a no arbitrage assumption, the present value of the pay off will equal the net premium paid.

Butterfly Spread(with call options)

Butterfly Spread(with put options)

Calendar Spread(with call/put option)

- Short 1 T 1 T_1 T1? call/put + Long 1 T 2 T_2 T2? call/put

- T 1 < T 2 T_1<T_2 T1?<T2?

- Calendar spread has a long and a short position with exercise price, but the maturity of long position is longer than that of short position.

3. Combined Strategies

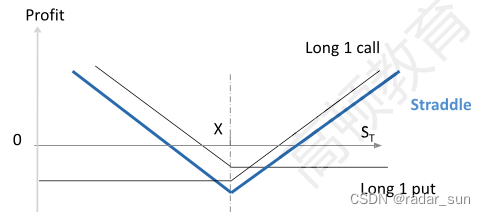

Straddle

- Long 1 call + long 1 put, both at X

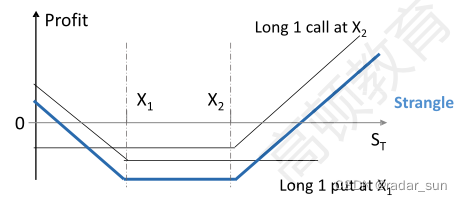

Strangle

- Long 1 call at

X

2

X_2

X2?+ long 1 put at

X

1

X_1

X1?, usually

X

1

<

X

2

X_1<X_2

X1?<X2?